The disproportionate impact of large-scale price events (LSPEs): nothing comes even close...

Key Markets report for Friday, 20 March 2026

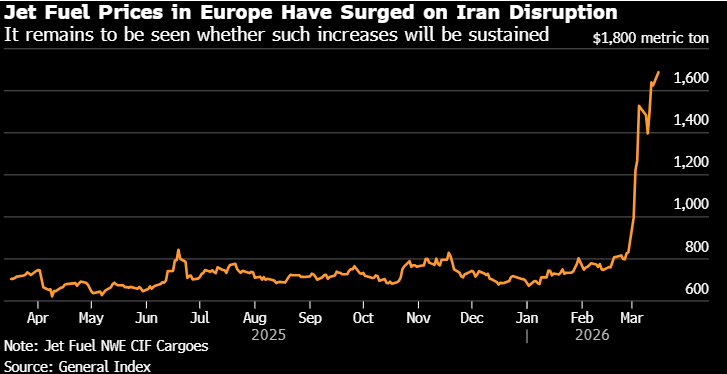

One of the most disruptive side-effects of the escalating geopolitical conflicts is an increasing volatility in commodity prices, which cold become part of our “new normal” for a good long while. This will inevitably have a dramatic impact on a range of industries in the whole global economy. In fact, it is hard to see how anyone - governments, industries or households - could avoid feeling the impact of these changes in their own lives.

Take the example of airlines. Reportedly, most airlines have not hedged their exposure to jet fuel prices, leaving them vulnerable to price risk when this happened:

To appreciate how disruptive these price dislocations tend to be, here are just some of the examples from April 2020 when the oil price collapsed by about 65% on the back of the public health response to the PCR test pandemic that year.

RyanAir hedged their exposure to jet fuel prices and lost $325 million on those positions.

Hin Leong, one of Asia’s largest oil traders did not hedge their exposure and lost $3.8 billion.

Vitol also didn’t hedge and lost $1.6 billion.

ABM Amro bank lost $1.4 billion

In the US, 25 independent oil producers filed for bankruptcy.

In 2022, oil prices soared to $120/barrel. That time, most of the independent U.S. shale oil producers did hedge their price exposure. As a result, they capped their production prices at about $60/bbl and sustained over $10 billion on their hedging positions.

Price is key

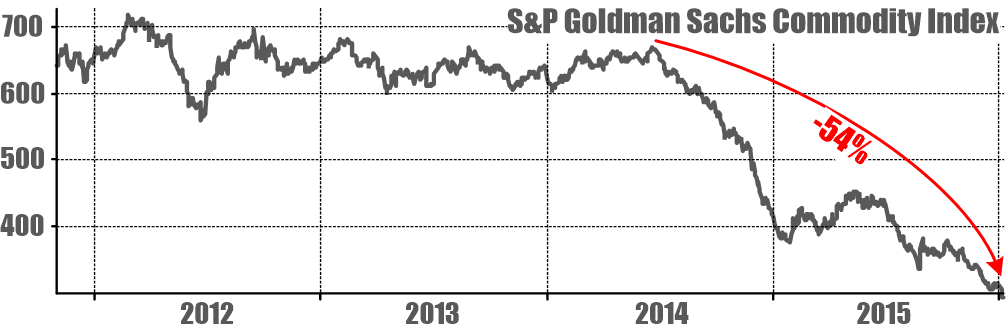

Price exposure represents far and away the greatest source of risk for firms with commodity price, currency or significant interest rate exposure and the incidents listed above happen all the time. Literally, nothing else comes close to the impact of price at which their sell their products or the cost of key inputs. One of the most instructive cases proving this principle took place in 2014/2015 when commodity prices collapsed by over 50%:

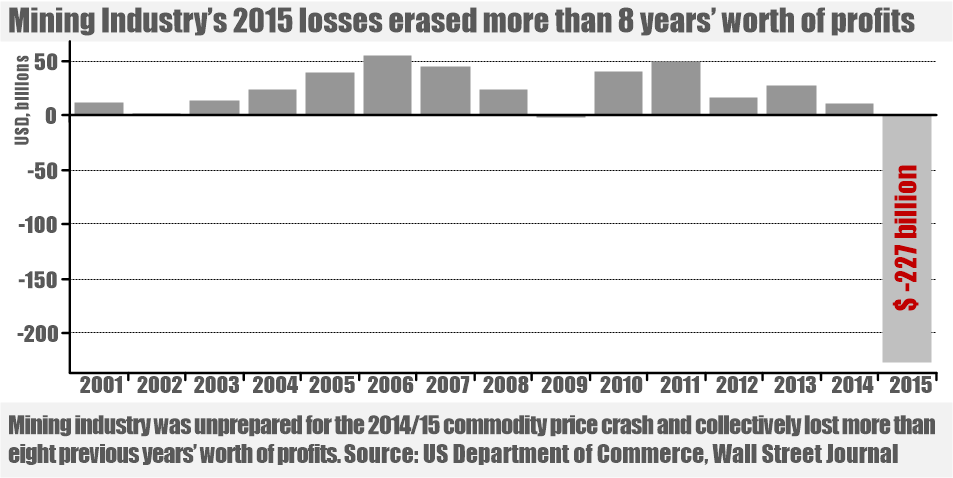

This event was disastrous for the mining industry, resulting in a total after-tax loss of $227 billion for 2015, wiping off more than eight years’ worth of industry’s profits:

This is why managing price risk could be the single most important determinant of profitability for commodity-related businesses. This is, in fact, widely recognized by managers in such companies: 90% of CEOs and CFOs believe that managing price risk is key to competitive advantage. For some reason however, they seem to keep failing to solve that key challenge: only 1/3rd of them have confidence in solutions they have in place. [1]

For this reason, every large-scale price event tends to create havoc among commodity producers and other firms with significant price exposure. That includes also financial institutions who have exposure to the price of money (interest rates). Presumably, they have a certain expertise in managing risk in financial markets, and make billions of dollars every year selling risk management solutions to their clients. In practice, however, they seem to be just as bad at managing price risk as anyone else.

When interest rates soared in 2022 and 2023, large banks like Silvergate, Signature Bank, Silicon Valley Bank and First Republic Bank all failed. The too-big-to-fail banks are no better at managing risk, but when they rake up losses, they routinely get bailed out with taxpayer money, which is the only reason we don’t see them fail as frequently as ordinary businesses and smaller banks do.

It’s trends, stupid!

One of the key mindset barriers to effective risk management (and this is the same mindset barrier obstructing effective investment performance) is in failure to recognize that large-scale price events always unfold as trends. Managing price risk could be as simple as hedging price exposure during unfavorable market moves and keeping that exposure during favorable moves. For example, oil producers could keep their production unhedged during oil bull markets and hedge during bear markets.

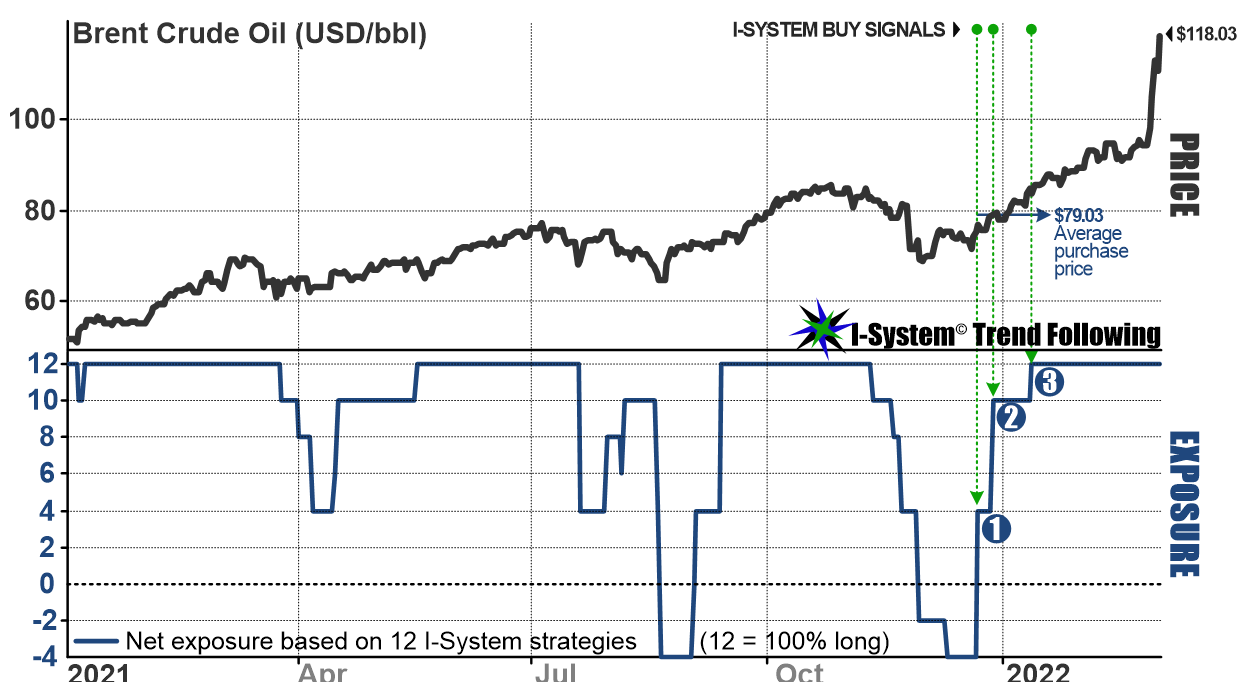

That may sound unrealistic and impossible to do in practice, but adhering to effective trend following strategies can do the trick, at least well enough to afford a company an important degree of protection against adverse price changes as well as a hard-to-duplicate competitive advantage over their rivals. A few days ago, I shared the trading signals generated by I-System strategies over the last two months: they all switched from short to long at an average price of $66.08.

A very similar situation played out during the 2021-2022 bull market. The signals generated by the exact same 12 strategies, from an earlier TrendCompass report is below:

We can see that our exposure switched from a net short position to a full, 100% long position in December 2021 and January 2022. Those signals were not based on any prediction; they were simply reactions to market price fluctuations as they happened and the assumption that markets move in trends: if prices are moving hither, we buy; if they are falling, sell. This works when trends unfold.

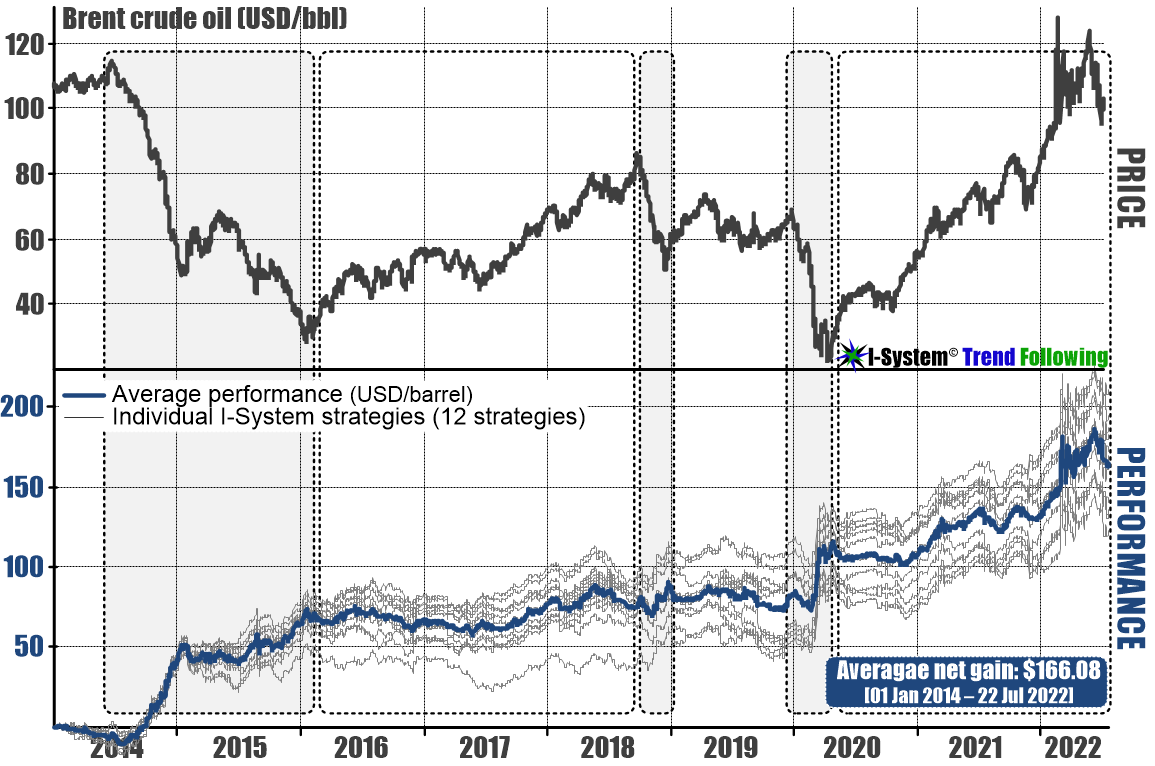

Here is how the same 12 strategies navigated over the longer term, spanning the 2014/15 crash that struck the mining industry as we saw above, and subsequent LSPEs:

In spite of long stretches of flat or negative performance, we can see that trend following tends to be effective at capturing windfalls from large-scale price events. During the tumultuous 9 years in the above chart, the average I-System strategy captured more than $160/bbl. This should not be a surprise because the same phenomenon that represents the largest source of risk must also represent the largest source of potential profit.

The trick is to formulate an effective strategy to manage that risk and to adhere to it with the requisite discipline and patience. This applies to managing price risk in exactly the same way as it applies to investment management. In both cases, LSPE’s are the most significant source of potential gains, which is very consistent to the twin hypotheses that form the foundation of I-System Trend Following:

Market trends are far and away the most powerful drivers of investment performance,

Systematic trend following is the most reliable way to capture value from trends.

That’s what this newsletter seeks to provide. Equally important are the discipline and patience required through the process. Unfortunately, we can’t provide that part: that’s always up to the practitioner.

Notes

[1] Tevelson, Robert, Petros Paranikas, Harish Hemmige. “Key Challenges in Managing Commodity Risk.” BCG Perspectives, 11 April 2013.

To learn more about TrendCompass reports please check our main TrendCompass web page. We encourage you to also have a read through our TrendCompass User Manual page. For U.S. investors: an investable, fully managed portfolio based on I-System TrendFollowing is available from our partner advisory (more about it here).

Today’s trading signals

With yesterday’s closing prices we have the following changes for the Key Markets portfolio: