Protecting your wealth against inflation

Key Markets report for Thursday, 24 June 2026

The noose is tightening on your organization, vast amounts of money printing are now required to keep your manipulated economy afloat. It will ultimately result in huge price inflation, or, if you stop printing, another massive economic crash will occur. There is no other way out.

Late, great economist Robert Wenzel in a speech at the NY Fed, April 2012

Further to yesterday’s report, I wanted to follow up with a discussion of the most effective ways available to investors to protect their wealth against the ravages of inflation. Consumer price inflation entails a progressive erosion of the purchasing power of the currency. Normally, the process also involves a corresponding rise in the prices of real assets: commodities such as oil, natural gas, copper, silver, wheat, coffee or cotton. It follows that exposure to the prices of such commodities could offset some of the loss of money’s purchasing power. This claim should be intuitive, but a good deal of empirical evidence also strongly supports it.

CTA/Managed Futures as inflation hedge

The types of investment funds that systematically trade a broad range of commodities are called Commodity Trading Advisors (CTAs) or Managed Futures funds. These investment vehicles offer investors exposure to commodity prices without having to own the real stuff which, apart from such assets as gold and silver, would be impracticable. CTAs also typically rely on trend following strategies to deliver performance. I have listed some of the most popular funds available to investors in the bottom of this report.

Over the recent decades, CTAs have proven particularly effective during periods of high inflation as well as bear markets in stocks and bonds. Below, I summarized the findings of seven analysis reports that looked at the performance of CTAs or trend following strategies during inflationary periods.

1. Abbey Capital

A 2011 paper by Abbey Capital’s J. Twomey, J. Foran and C. Brosnan presented an authoritative analysis of the performance of CTA/Managed Futures investments over a 31-year period from 1980 to 2011, comparing it with other asset classes like equities, bonds, commodities and gold. The authors concluded that,

Managed futures outperform the other asset classes, returning almost 70 times the original investment in January 1980. … No other asset class presents itself as a viable inflation hedge.

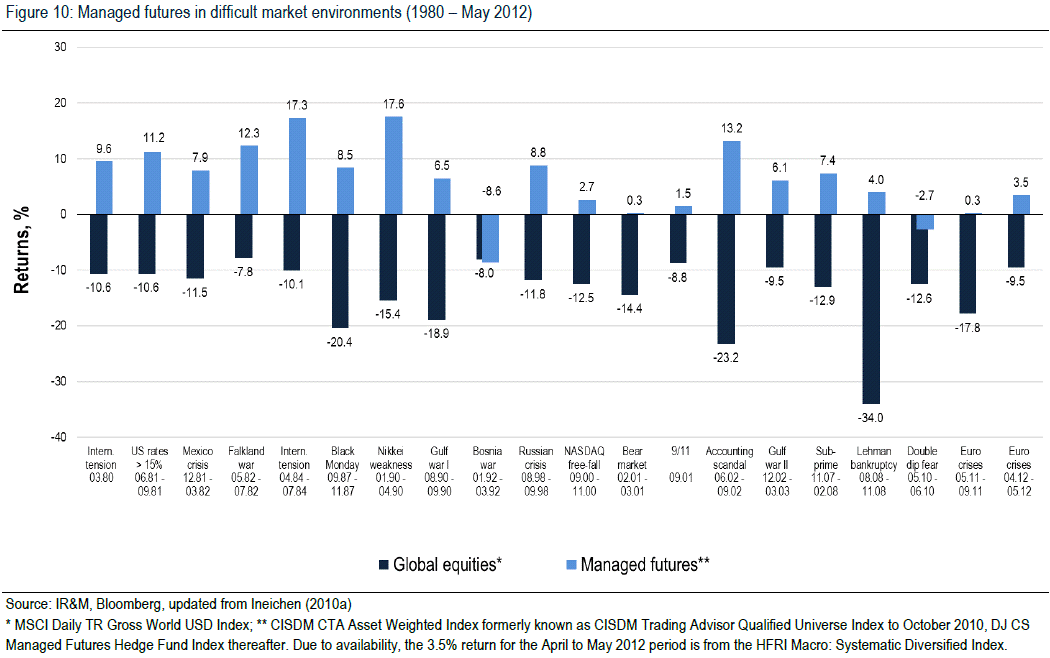

2. Ineichen Research

Another report, by Ineichen Research and Management (June 2012) analysed the portfolio hedging properties of gold, equities and hedge funds, as well as individual hedge fund strategies between 1980 and May 2012.

Ineichen looked at the occurrence of “financial accidents” where the MSCI World Index lost more than 7% of its value within one, two, three, or four months and identified 18 such accidents over the observed period. They found that,

Managed futures delivered a positive return in 18 out of 20 accidents in the equity market. In the field of investment management, there is simply nothing that comes anywhere close to this. … Gold only delivered a positive return in eight out of the 20 identified accidents.

Further, Ineichen analysis took into account overlapping 5-year total returns for CTA/Managed Futures, global equities, global bonds and a 50/50 balanced portfolio of bonds and equities:

… managed futures outperformed the balanced portfolio in ten out of 13 (overlapping) 5-year periods. It outperformed global bonds in all occurrences except the five-year period to 2011. Managed futures outperformed global equities in 17 (61%) out of 28 five-year periods. It has always outperformed equities when the latter’s return was smaller than 7.7%.

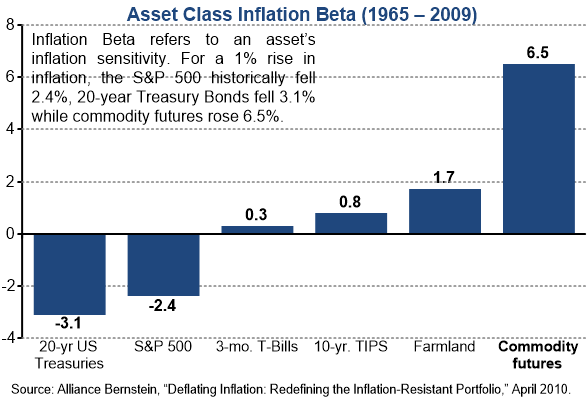

3. Alliance Bernstein

An analysis report by Alliance Bernstein titled, “Deflating Inflation: Redefining the Inflation-Resistant Portfolio” (2010) found that of all asset classes, managed futures had the highest inflation beta (explained in the below graphic):

4. Neville et al.

In their paper, ‘The Best Strategies for Inflationary Times,’ Neville et al. reviewed inflationary episodes in the U.S. between 1926 and 2021 and compared the performance of diversified trend following portfolios to other major asset classes, namely commodities, equities, US Government bonds and the traditional 60/40 portfolios.

They found that trend following portfolios showed significant outperformance over other asset classes, all of which provided poor protection from inflation. They conclude that trend followers are likely to be well-suited to future inflationary environments.

5. Quantica research

A research report by Quantica analyzed the performance of trend following portfolios through inflationary periods since 1962 and found that, “Every crisis creates trends… a generic trend following strategy provides attractive smart diversification against inflation risk…”

6. Gorton and Rouwenhorst

Finally, an older (2004) paper by NBER’s Gary Gorton and Yale’s K. Geert Rouwenhorst analysed the 43-year period from 1959 to 2003 and identified seven boom-and-bust cycles. They concluded that commodity futures investments tended to reduce overall risk of loss in an investment portfolio, particularly during periods of recession and inflation.

Big vs. small CTAs

CTAs gained greater recognition and legitimacy thanks to their performance during the 2000 and 2008 market busts. As a result, some of the leading CTAs grew to become fairly large funds, managing upwards of $10 or even $20 billion in assets. At that size, they became a very different animal from smaller CTAs. Traditionally, CTAs represented a very niche investment strategy. They were relatively small (sub-$1 billion) and tended to rely fairly heavily on commodity markets to generate investment returns.

For the very largest CTAs, this has become next to impossible as they are simply too large to meaningfully participate in the commodity futures markets. For example, one large CTA (Winton) concentrates over 70% of their risk in interest rate/treasury futures and less than 10% of risk in commodities futures. With only a token participation in commodities markets, their ability to generate upside performance from inflation, and provide investors an effective inflation hedge could be limited. Having said that…

The likely bonds armageddon and CTAs

However, as I wrote in this newsletter in the past, I believe that one of the consequences of the coming crisis will also be a significant decline in bonds prices, which will likely benefit the large players with large allocations to bonds. Because CTAs, as a rule, are trend followers and trade securities both on the long and on the short side, they should be able to generate positive returns from a bear market in bonds.

In the past, I didn’t use to recommend large CTAs as a valid inflation hedge, but I changed my mind about that over the bonds armageddon scenario, so the list of the most legit investment vehicles available to investors is as follows:

Man AHL (e.g., Man AHL Alpha / Evolution / Dimension programs) with over $25 billion in systematic managed futures strategies. A core constituent of the SG Trend Index.

Winton Capital Management (e.g., Winton Trend Fund / Futures Program): cca. $18 billion in assets under management. Known for medium-term trend-following; offers UCITS and other accessible vehicles.

Two Sigma (e.g., Compass): Roughly $15 billion in relevant trend-following assets.

Aspect Capital (e.g., Aspect Diversified): About $12 billion.

Graham Capital (e.g., Graham Systematic / Tactical Trend): Around $10–11 billion.

Others notable: Campbell Systematic (~$9 billion), Transtrend, Lynx Asset Management, AQR, and Systematica (BlueTrend).

These managers frequently appear in benchmarks like the SG Trend Index, which tracks the 10 largest trend-following CTAs open to investment. Recent constituents include Man AHL Alpha, Winton Trend, Aspect, Graham, AQR, Transtrend, Lynx, and others.

For retail investors, mutual funds and ETFs provide easier access to the strategy without high minimum investments or accredited investor status:

Mutual Funds: AQR Managed Futures Strategy (AQMNX), American Beacon AHL Managed Futures (AHLAX), Abbey Capital Futures Strategy, Arrow Managed Futures (MFTFX), and others.

ETFs: Simplify Managed Futures Strategy (CTA), iMGP DBi Managed Futures (DBMF — replicates top CTAs), Invesco Managed Futures Strategy, WisdomTree Managed Futures (WTMF), and KFA Mount Lucas (KMLM). These have grown in popularity for liquidity and lower costs.

Last but not least, in partnership with Capital Investment Advisers we propose two Trend Investing Models (description at link).

Please note, however: over the recent years, CTAs have had fairly mixed performance results - very strong in some years, but lackluster in others. The reason for this is that market fluctuations dynamics have changed over the last two decades or so. However, CTAs and trend following funds have continued to deliver uncorrelated returns, particularly during equity bear markets. They also had strong positive returns during the inflationary 2021/2022 period, suggesting again that the strategy remains the single most effective hedge against inflation.

Lastly: if farmland is an option, it represents the second most effective inflation hedge, as per the “inflation beta” chart above.

To learn more about TrendCompass reports please check our main TrendCompass web page. We encourage you to also have a read through our TrendCompass User Manual page. For U.S. investors: an investable, fully managed portfolio based on I-System TrendFollowing is available from our partner advisory (more about it here).

Today’s trading signals

With yesterday’s closing prices we have the following changes for the Key Markets portfolio: