Could Japan set off a stock market tsunami?

Key Markets report for Tuesday, 13 May 2025

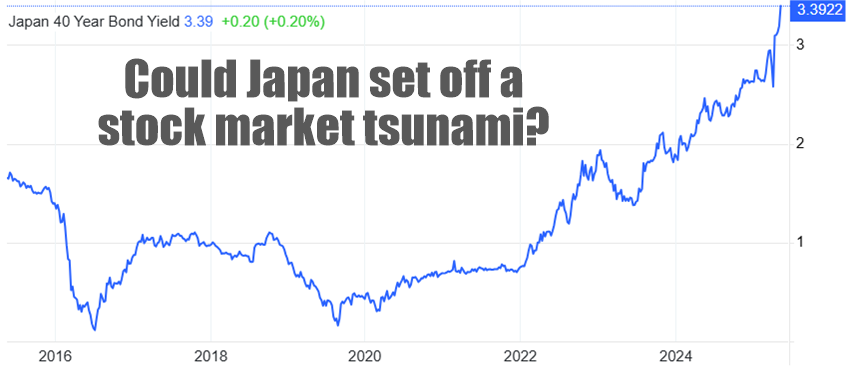

Last week, Japan’s 40-year government bond yield surged to nearly 3.4%, its highest level in over two decades - a development which could trigger an avalanche for the entire global financial system. For decades, the Bank of Japan ran a policy of financial repression by keeping interest rates artificially low in order to keep its staggering 260% debt-to-GDP ratio manageable.

Effectively, the BOJ has been monetizing government debt as the permanent buyer of last resort. As a result, it now owes nearly half of all Japanese Government Bonds (JGBs). Of course, the situation was unsustainable and the last two years' surge in yields indicates that the BOJ may be losing control of the bonds market, or that it is effecting a deliberate policy shift in order to defend the yen.

Governor Ueda could be allowing long-term yields to rise in order to strengthen the yen without directly intervening in FX markets and selling BOJ's dollar reserves. Higher interest rates in Japan will narrow the interest rates gap with the US, and help strengthen Japanese currency. As the yields rise, the price of long-dated bonds is crashing which could have severe adverse impact on Japanese life insurers and pension funds who are heavily invested in long-dated government bonds.

Will we see a global contagion?

The surge in yields could also impact global financial markets if Japanese institutional investors begin repatriating the capital invested abroad at scale to take advantage of higher bond yields at home. This could, in turn, trigger significant selling pressure on US and European treasuries, pushing yields in those markets higher, which could be particularly destabilizing for the US economy, given that Japan is still the largest foreign holder of US treasuries.

Ultimately, this could lead to a rise in interest rates across the board, causing tighter financial conditions globally and exerting further pressure on global equity markets, including Japanese and American stocks. In fact, these conditions are similar to what we experienced during the 1998 Japanese bond market crisis. At that time, a sharp surge in Japanese yields triggered significant losses for global funds that were heavily leveraged into carry trades. The difference between 1998 and today is that the scale of the risk is much higher and Japan's economy is significantly more fragile.

Sacrifice the economy to save the currency?

The conditions reflect central banks’ dilemma between stimulating the economy and defending the currency. One of the main objectives of keeping interest rates artificially low is to stimulate the economy. But this ultimately weakens the currency. However, allowing interest rates to rise can suffocate the economy, particularly if it carries too much debt. The collapse of bond prices could itself destabilize the financial system because government bonds usually represent the collateral against which the banks can issue loans.

If the collateral pool shrinks, banks can be forced to curtail credit and call in loans, setting off a self-reinforcing deflationary spiral, an economic depression and a bear market in stocks. As ever, warning signs are out there, but predicting the coming sequence of events with any degree of accuracy is out of the question. Instead, the more reliable approach to navigating these changes is by adhering to high quality trend following strategies, which is the ultimate purpose of this newsletter.

To learn more about TrendCompass reports please check our main TrendCompass web page. We encourage you to also have a read through our TrendCompass User Manual page. For U.S. investors: an investable, fully managed portfolio based on I-System TrendFollowing is available from our partner advisory (more about it here).

Today’s trading signals

With Friday’s closing prices we have the following changes for the Key Markets portfolio:

Keep reading with a 7-day free trial

Subscribe to I-System TrendCompass to keep reading this post and get 7 days of free access to the full post archives.